The Wealth Management industry has a problem, and it's not the one it thinks it has. While firms have been busy obsessing over Gen Z's digital habits and Gen Alpha's eventual inheritance, a far bigger shift is already happening, and most of the old school firms are completely unprepared for it.

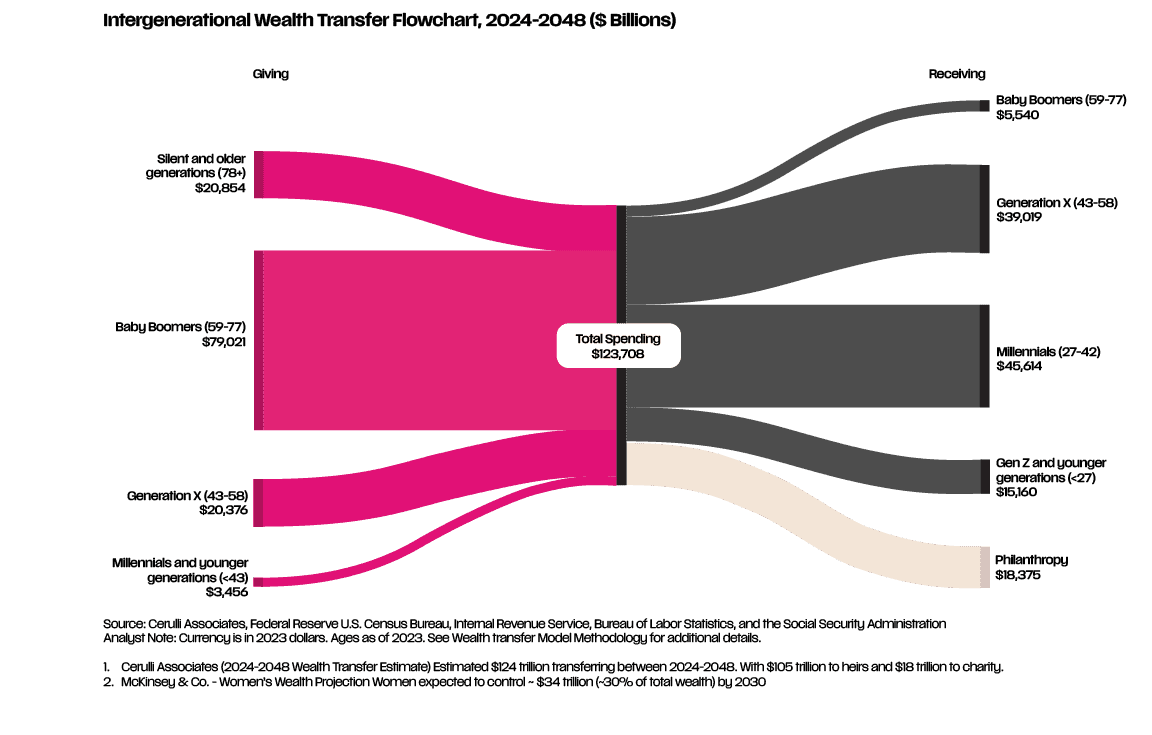

We are in the middle of a $124 trillion wealth transfer, the largest recapitalisation in financial history. And because women outlive men, the first $54 trillion isn't going to the kids - it's going sideways, to women. Women who have watched their financial advisors spend decades talking to their husbands, and who are often seen as a plus-one in their own financial lives. The result? Approximately 70% of women fire their financial advisor within a year of their husband's death.

Not because they're grieving and distracted. Because the relationship was never actually with them. The Old Guard built those relationships with men, and now those men are gone, and so shortly is the money.

Inheritance is only part of the story. Women are building wealth like never before, founding companies, reaching the C-suite, and driving liquidity events. And more than half of them are doing it completely unadvised because they look at the industry and don't see anyone who looks like them, thinks like them, or recognises them. That’s the reality.

The firms that make it through the next thirty years will be the ones that figure this out. The ones that don't are already losing assets, and some of them know it.

By 2048, nearly $40 trillion will go to widowed Baby Boomer women, the generation that is quietly becoming the primary holder of global family wealth. In the UK alone, the transfer is expected to hit £7 trillion by 2050, with women already 45% more likely to have inherited assets than the generation before them. By 2030, women are projected to control roughly 40% of global investable wealth, around $46.3 trillion. That's not a niche market. That's pretty much half the market.

An industry ignoring the other half

Eye-tracking studies during joint advisory sessions found that advisors spend, on average, 60% of their time focused on the male spouse even when women often function as the ‘CFO’ of their families. The eye watering cost of this demographic blindness is estimated at $700 billion annually, a global revenue opportunity modelled by Oliver Wyman across wealth management, retail banking, commercial lending, and insurance, representing what firms really leave on the table by failing to serve female clients as a primary audience.

Founders and the funding gap

Women are starting businesses at 1.5 times the national average. Not lifestyle businesses but technology companies, healthcare ventures, and fintech. The kind that end in acquisitions and require serious, sophisticated financial planning well before the exit.

Traditional private banks miss almost all of this. They're built for wealth that already exists and is sitting still. Female founders need partners who can help them during the messy, high-growth, pre-liquidity phase and the industry mostly isn't there. The banks that show up early, with genuine support, not just a brochure, are the ones that will manage the wealth on the other side of their pre-planned exit.

Key themes emerging around wealth for women

Career flexibility. For a lot of senior women, wealth isn't about the number accumulating. It's about options and the ability to walk away from a job they hate, to pivot, to take a risk without financial catastrophe. Millennial women are 38% more likely to define wealth as the freedom to move, compared to just 16% of older women.

ESG is not a soft preference. 64% of women always factor ESG considerations into their investment decisions. Always - not sometimes, or when asked. For many female investors, ESG alignment is a baseline requirement for trust. After watching institution after institution fail, hide things, and wriggle out of accountability, their bar for trust is not low, it’s reasonable. Gender-lens investing has become its own discipline: investing for women (products built around women's real needs), investing in women (backing companies with gender-diverse leadership), and investing by women (directing capital to female-led ventures).

Diligent, not risk-averse. A 2025 study, Are Women More Risk Averse? A Sequel, went back through the data and found no significant gender difference in financial risk aversion among never-married households. Both men and women increase their exposure to risk as their wealth grows, at roughly the same rate. What women do differently is due diligence, they ask more questions and want to understand what they're actually buying.

Philanthropy is a strategy, not generosity. 61% of Millennial women plan to give away significant wealth during their own lifetimes rather than leave it to an estate, nearly twice the rate of Boomers or Gen X. These are intentional decisions, aligned with tax planning, estate structures, and measurable impact outcomes.

Giving circles, collaborative philanthropy pools where individuals aggregate resources for community-level impact, have tripled between 2016 and 2023. MacKenzie Scott who sold her Amazon stake has donated $26 billion since 2019 - she has redefined what major philanthropy can look like. Firms treating philanthropy as a year-end tax conversation are going to lose these relationships, and they'll never fully understand why.

A reality. Not the future.

This is not a trend piece about the future. This is about what is happening right now. The money is already moving. Nearly half of all wealth management firms have identified wealth transfer as a risk, which means they see it and they understand what it means.

But is enough being done?

The Lindy Effect says that what has survived for 200 years will survive for 200 more. Fine, in a stable world. But we're not in a stable world. We're in a world of agentic AI, open banking, and a generation of women who have built genuine wealth, know exactly what they want, and have no patience for institutions that treat them like an afterthought.

The firms that will be standing in thirty years are the ones that recognise women as the primary clients and not the spouses of clients. Those who build technology that gives them real agency over their money. Those that offer ESG products that are actually good, not just good-looking. Those will be the firms that thrive.

Longevity isn't earned by sounding timeless. It's earned by being relevant right now, and always. The money is moving. The only question is whether these institutions have the imagination and the urgency to follow it.

Sources

[1] Cambridge Trust — Women & The Great Wealth Transfer [2] The American College of Financial Services — The Future Client is Female (2023) [3] Morgan Stanley — SHEconomy: Women's Wealth Shift [4] RBC Wealth Management — Women's Economic Power Survey (2026) [5] Merrill Lynch Wealth Management — Seeing the Unseen: The Role Gender Plays in Wealth Management (2020) [6] WealthBriefing / HSBC — Private Banks Missing $100 Trillion Opportunity [7] Oliver Wyman — Women in Financial Services (2020) [8] CAIA — The Great Wealth Transfer: An Opportunity for Female Financial Advisors (2025) [9] WEF — Transforming Capital for the Next Era (2025) [10] MDPI Risks — Are Women More Risk Averse? A Sequel (2025) [11] InvestmentNews — How Women Are Redefining Modern Philanthropy [12] Mercer Advisors — Women in Philanthropy: Expanding Leadership, Impact, and Global Giving